- Low Credit Score

- Debt-to-Income Ratio Issues

- Incomplete or Incorrect Documentation

- Valuation Concerns

- Age Restrictions

- FAQs

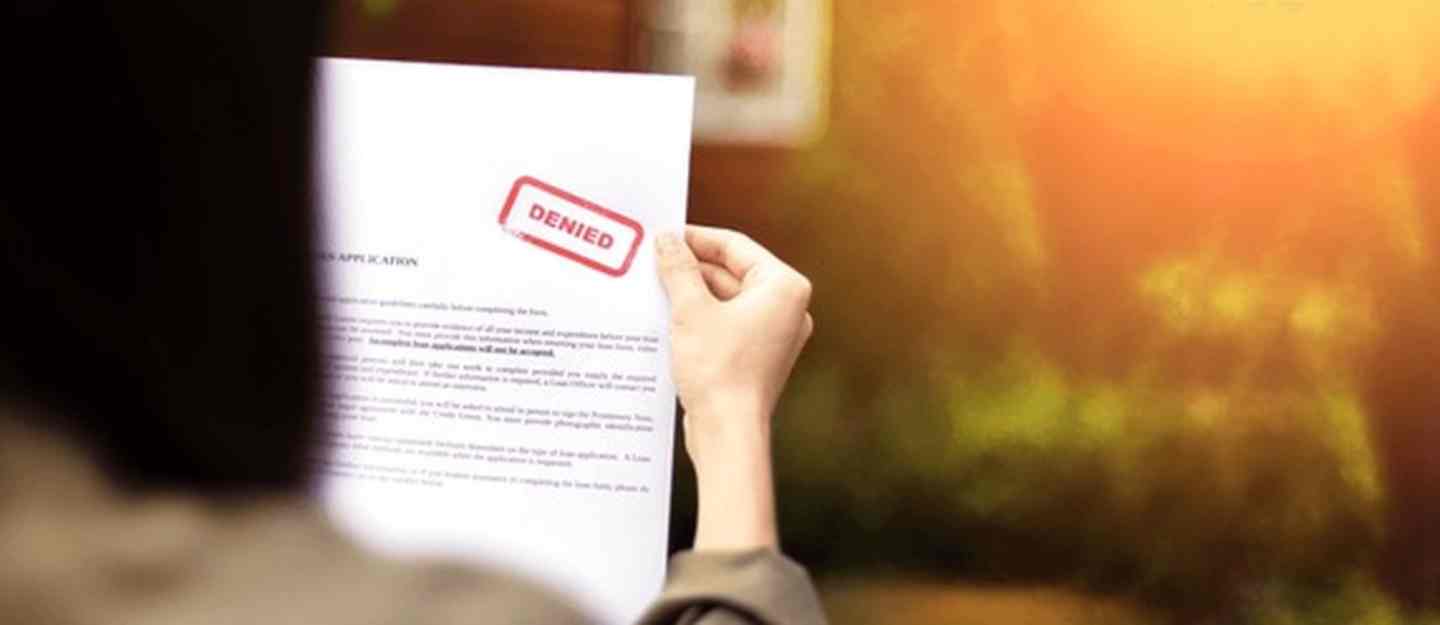

Mortgage applications in the UAE are often subject to strict criteria and many applicants find their requests rejected despite meeting the basic requirements. Understanding the reasons for mortgage application rejection can help individuals and families navigate the process more effectively. While the specific factors may vary depending on the lender, there are common elements that could lead to a denial.

Reasons For Mortgage Application Rejection

In addition to financial factors, the UAE’s dynamic property market and shifting regulations can also influence mortgage approval. Understanding these external factors is crucial when applying for a mortgage in the UAE.

Detailed below are some common mortgage rejection reasons in the UAE.

Insufficient Credit History or Low Credit Score

A key factor influencing mortgage approval or mortgage refinancing in the UAE is the applicant’s creditworthiness. Banks and financial institutions assess credit scores to gauge the risk of lending. A low credit score, often resulting from missed payments or insufficient credit history, can lead to a rejection.

Foreign nationals, especially those with a limited credit history in the UAE, may find it particularly challenging to secure a mortgage. It is essential to review and improve credit scores before applying for a mortgage.

Debt-to-Income Ratio Issues

The debt-to-income (DTI) ratio is a crucial consideration for UAE banks. This ratio measures an applicant’s monthly debt payments relative to their monthly income. A high DTI ratio signals that the applicant may already have too many financial obligations to manage an additional loan.

Most lenders in the UAE require the DTI ratio to remain within a specified limit, often around 50%. Those exceeding this threshold may find their mortgage applications rejected due to the perceived risk of default. Be sure the ratio fits the criteria when applying for a home mortgage in Dubai, Abu Dhabi or any other emirate.

Incomplete or Incorrect Documentation

One of the reasons for mortgage application rejection is the submission of incomplete, incorrect or fraudulent documentation. Lenders require comprehensive documents, including proof of income, residence, identification and financial statements, to assess the application.

Inaccuracies or omissions in these documents can delay the process or lead to outright rejection. Applicants need to ensure all required documents are correctly prepared and submitted to avoid unnecessary complications.

Property Type and Valuation Concerns

The type of property to be purchased can also influence a mortgage application outcome. Lenders may be hesitant to finance properties in certain areas or types of developments that do not meet their criteria. For instance, off-plan properties or those located in less desirable regions may be viewed as higher risk. Additionally, if the property’s valuation comes in lower than the sale price, the bank may reject the application due to concerns about the value of the collateral.

Age Restrictions

Age restrictions are another important factor that can lead to mortgage rejection in the UAE. Most lenders have specific age limits, typically requiring applicants to be between 21 and 60 years old at the time of application. This ensures that the borrower has sufficient time to repay the mortgage before reaching retirement age.

FAQs

Why are mortgage applications commonly rejected in the UAE?

Factors of home loan application rejected in the UAE include low credit scores, unstable income, high debt levels, incomplete documentation, property concerns and age restrictions.

How does a credit score affect mortgage approval in the UAE?

A low or insufficient credit score reduces lender confidence in repayment ability, making mortgage approval less likely.

Can a high debt burden ratio cause mortgage rejection in the UAE?

Yes, a high debt ratio is among the UAE home loan rejection. It signals that the applicant may already be financially overextended.

There you have it, the common reasons for mortgage application rejection in the UAE. Potential applicants should thoroughly assess their creditworthiness, ensure stable income, maintain a manageable debt load and submit accurate documents to increase their chances of approval. By understanding and addressing these common pitfalls and bank mortgage criteria in the UAE, individuals can significantly improve their prospects of securing a mortgage.

There are also some handy tips to avoid mortgage rejection that applicants should follow. Moreover, weighing the pros and cons of buying a property on a mortgage or cash can also help make a more practical decision.

The many new projects in the UAE can be formidable choices for end-users and investors alike. Many developers also have offers on their properties.

Stay tuned to dubizzle’s property blog for information about home mortgages in the UAE and more.